Whirlpool, the traditional powerhouse of the American home appliance industry, is struggling to regain its competitive edge despite steep protective tariff barriers. Once the undisputed leader in the United States, Whirlpool's market share across core appliance categories has slipped to fourth place. While import tariffs were expected to hand the domestic giant a structural advantage, its market share has remained largely stagnant, pushing the company into a prolonged downturn marked by mass layoffs and factory closures.

According to market tracker Traqline, Whirlpool's revenue-based market share across six major appliance categories--refrigerators, washing machines, dryers, dishwashers, freestanding ranges, and microwaves--stood at 14.3% last year, a 1.5 percentage point drop from 15.8% in 2015, a slide that pushed the company from first to fourth place over the decade.

The refrigerator segment, which was projected to be a primary beneficiary of U.S. tariff protections, showed a similar pattern. Traqline data put Whirlpool's refrigerator market share at 13.2% last year, a modest 0.3 percentage point increase from the previous year's 12.9%. The uptick was barely enough to arrest a downward spiral that has persisted since 2020.

Industry analysts view Whirlpool as having entered a phase of structural stagnation. Back in 2015, the market share gaps among the top four players in the U.S. major appliance market--Whirlpool, GE, Samsung Electronics, and LG Electronics--were remarkably tight. But as the upper tier of the market underwent a massive reshaping over the following decade, Whirlpool failed to hold on to even its decade-old position.

This underperformance was clearly reflected in the company's first-quarter earnings. Despite prioritizing a turnaround in North American profitability through price hikes, cost-cutting measures, and footprint optimization, Whirlpool's first-quarter revenue slid 9.6% year-over-year to $3.3 billion. By contrast, South Korean competitors, which bore the direct brunt of the import tariffs, saw their revenues climb over the same period.

Whirlpool has also struggled to capitalize on its policy-driven advantage. In its financial reports, the company estimated the net benefit of tariff policies at roughly 5% of revenue, while competitors faced a negative headwind of about 10% to 15% of revenue. Despite this clear regulatory edge, Whirlpool has remained focused on price increases--enacting its steepest hike in a decade this past April--alongside cost-saving measures and footprint restructuring.

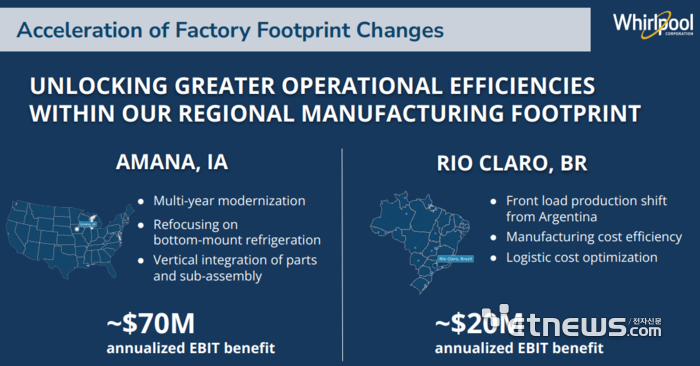

The financial strain has triggered aggressive downsizing. According to Reuters, Whirlpool laid off more than 1,000 workers at its Amana, Iowa refrigerator plant last year. An assembly line capable of producing 1 million refrigerators annually is now reportedly running at just 20% capacity. The manufacturing reshuffle extends beyond U.S. borders: Whirlpool has finalized plans to shutter a refrigerator production facility in Mexico by the second quarter of next year.

The global home appliance industry views Whirlpool's decline as a cautionary tale. While South Korean appliance manufacturers currently maintain an edge in the global market, Chinese rivals are rapidly closing the gap across all major white goods categories. Experts argue that if industrial policy relies solely on protectionism or subsidies without driving core innovation, domestic champions risk falling into stagnation, echoing the fates of Whirlpool or legacy Japanese electronics giants.

“Tariffs can lower the price competitiveness of imports to buy domestic companies time, but they cannot substitute for product quality, cost competitiveness, or brand preference,” an industry insider noted. “Erecting protective barriers after being overtaken by fast-moving Chinese rivals is simply too little, too late.”