Preemptive Response to Risks of Tightening U.S. Regulations

Photoresist Strip and Rapid Thermal Processing Equipment

Samsung and SK Hynix Review Alternative Suppliers

Competitive Movements Between Global and Korean Firms

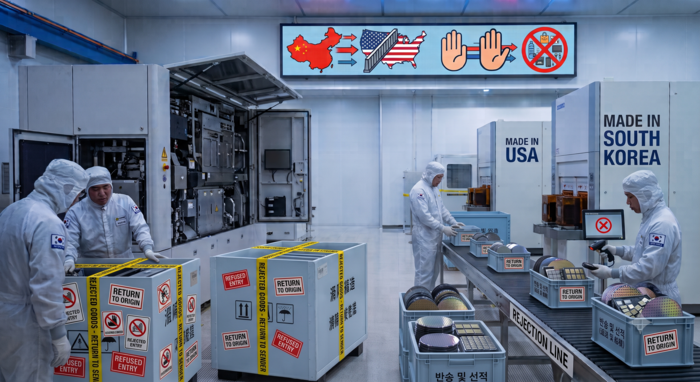

Samsung Electronics and SK Hynix have embarked on reorganizing their semiconductor materials, components, and equipment supply chains, which heavily rely on China. It is understood that they are pushing for plans to replace some Chinese equipment with products from other countries, such as South Korea and the United States, in order to preemptively respond to the possibility of the United States tightening regulations against China. The conflict between the United States and China appears to be shaking up even the supply chain landscape of domestic semiconductor manufacturing.

According to industry sources on July 5, Samsung and SK Hynix are pushing for plans to reduce the proportion of equipment introduced from China's Mattson Technology. Representative examples include photoresist (PR) strip equipment that removes photoresist residue and rapid thermal processing (RTP) apparatuses that apply high temperatures to wafers. Both types of equipment are areas where Mattson has secured a high market share, and many have been introduced into the production lines of Samsung and SK Hynix.

An industry insider familiar with the matter stated, “Currently, alternative suppliers to replace Mattson equipment are being reviewed for the new production lines of Samsung and SK Hynix. We are already discussing supply plans with domestic and foreign PR strip equipment and RTP companies.”

Mattson was originally an American semiconductor equipment company, but it was acquired by Chinese capital in 2016 and incorporated as an affiliate of Beijing E-Town Semiconductor Technology (E-Town). E-Town is a state-owned investment company under the Beijing Municipal Government, meaning that Mattson is currently virtually under the influence of Chinese state-owned capital.

The decision by Samsung and SK Hynix to replace Mattson equipment is interpreted as stemming from this background. Although Mattson has not yet been listed on the U.S. Department of Commerce's Entity List, the possibility that it could become a target of regulations in the future cannot be ruled out. Concerns are growing that if equipment or technology from a company on the Entity List is included in the supply chain, it could impact exports to the United States.

Previously, Taiwan Semiconductor Manufacturing Company (TSMC), the world's largest semiconductor foundry company, reportedly excluded equipment from Mattson and Advanced Micro-Fabrication Equipment Inc. (AMEC) from its manufacturing of advanced semiconductors, such as 2-nanometer chips, last year. This is interpreted as having removed factors causing production disruptions in advance, considering the possibility of the United States strengthening regulations on Chinese-made equipment.

In fact, it is reported that the proportion of Mattson equipment has also decreased in the recent introduction of new equipment by Samsung and SK Hynix. On the surface, there were evaluations that its performance and price competitiveness fell somewhat compared to competitors, but the industry also offers an analysis that it was a decision considering U.S. regulatory risks.

The supply chain reorganization movement is spreading beyond equipment into the components sector. It is known that when supplying components to Samsung and SK Hynix, requests are also being made not to share the same products with Chinese semiconductor manufacturers as much as possible.

The corporate body representative of a component company that supplies consumables for semiconductor processes to both companies said, “We received verbal requests stating that while trading with American or Taiwanese semiconductor companies is not heavily questioned, we should bring cooperation with Chinese manufacturers as cautiously as possible. While we used to worry about technology leaks in the past, the recent atmosphere places more weight on supply chain risk management.”

As decoupling from China takes place in some materials, components, and equipment supply chains, benefits are expected for traditional global companies ranked among the top five semiconductor equipment firms--such as Applied Materials, ASML, Lam Research, Tokyo Electron (TEL), and KLA--as well as domestic equipment companies.

The corporate body representative of a semiconductor equipment company noted, “Competition between global corporations and Korean enterprises has begun, targeting the demand to replace Mattson equipment. For some new equipment, preparations are even underway for domestic production.”