South Korean outsourced semiconductor assembly and test (OSAT) providers are gearing up for a strong rebound after a prolonged downturn. Fueled by the broader semiconductor market recovery, demand for back-end processing is rebounding sharply after being weighed down by a sluggish IT device market and client inventory corrections.

According to consensus estimates from major brokerages on July 6, leading domestic OSAT firms--including Hana Micron, SFA Semiconductor, Nepes Ark, and Doosan Tesna--are all projected to post year-over-year growth in revenue, operating profit, and net income for the second quarter. This sector-wide financial turnaround is being driven by rising memory prices, the industry's transition to DDR5, and increased testing volumes for automotive and artificial intelligence (AI) chips.

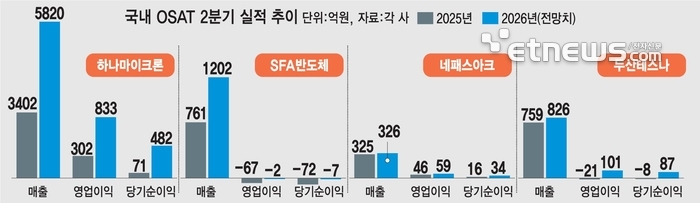

Hana Micron is poised to deliver the most explosive growth. The company's second-quarter revenue is forecast to reach 582 billion won, a staggering 70% increase compared to 340.2 billion won during the same period last year. Its operating profit is expected to nearly triple from 30.2 billion won to 83.3 billion won, while net income is projected to jump nearly sevenfold, from 7.1 billion won to 48.2 billion won.

Analysts attribute this surge directly to the rebounding memory sector. As a primary provider of DRAM packaging for major South Korean memory chipmakers, Hana Micron is benefiting from sharply higher average selling prices (ASPs) for finished memory products through its Brazilian subsidiary, coupled with strong advance-purchase demand from clients. The expansion of its manufacturing capacity in Vietnam is also providing structural tailwinds for revenue growth.

SFA Semiconductor is expected to remain in the red, but its losses are likely to shrink dramatically. Second-quarter revenue is projected to climb 60% year-over-year to 120.2 billion won. Meanwhile, its operating loss is forecast to narrow from 6.7 billion won last year to just 200 million won, and its net loss is set to contract from 7.2 billion won to 700 million won.

One-time expenses tied to relocating and installing high-value DDR5 testing equipment at its Philippine subsidiary may weigh on profitability through the second quarter. However, the ramp-up of these machines in the second half is expected to accelerate earnings recovery, particularly in premium products.

For Nepes Ark, the focus is on profitability rather than top-line growth. While its second-quarter revenue estimate of 32.6 billion won is effectively flat compared to last year's 32.5 billion won, its operating profit is projected to rise from 4.6 billion won to 5.9 billion won, and net income is set to more than double from 1.6 billion won to 3.4 billion won.

Doosan Tesna is anticipated to stage a decisive swing to profitability. Second-quarter revenue is forecast to grow roughly 10% year-over-year to 82.6 billion won. More importantly, operating profit is expected to turn around from a 2.1 billion won loss last year to a 10.1 billion won profit, while net income is projected to swing from an 800 million won loss to an 8.7 billion won profit.

“The back-end testing sector is experiencing a clear trickle-down effect,” noted Dong-kwan Kim, an analyst at Meritz Securities. “As foundry clients gradually see their own businesses recover, outsourced demand for chip testing is rising in tandem.”